I have been busy with paper writing recently and have not had time to post on my public account for a while, but I have continued reading. My most important recent gains come from reading David Swensen, former Chief Investment Officer of the Yale Endowment, Pioneering Portfolio Management, and Morgan Housel’s The Psychology of Money. In this memorandum I want to briefly discuss some of my thoughts on consumption and investment.

The Yale Model and Swensen’s Institutional Contribution

Most finance practitioners should be familiar with the Yale Endowment and David Swensen. Since taking office as CIO in 1985, Swensen systematically reconstructed the asset allocation framework for university endowments, gradually reducing dependence on traditional publicly traded stocks and bonds and substantially increasing allocations to alternative assets such as private equity, venture capital, hedge funds, real estate, and natural resources, forming the long-term investment paradigm later summarised as the “Yale Model.” Under his management, the Yale Endowment achieved robust compound returns across cycles and significantly improved risk-adjusted returns. Swensen altered institutional investors’ understanding of asset diversification and time horizons at the institutional level. The model was subsequently widely adopted by large institutional investors such as Harvard, Stanford, and sovereign wealth funds and pensions worldwide, and it has had a sustained and profound impact on modern institutional asset management theory and practice. His book Pioneering Portfolio Management systematically summarises his asset allocation ideas and governance logic. The book not only became a classic text for university endowment management but also has had lasting influence on pension funds, sovereign wealth funds, and high-net-worth asset allocation frameworks.

Reservations about Asset Allocation Theory

First, the parts of Pioneering Portfolio Management I disagree with. As an investor, I have long held reservations about the theoretical foundation of asset allocation. The basic logic of asset allocation derives from modern portfolio theory: under a given expected return, reduce portfolio volatility by diversification; or under a given risk constraint, increase expected returns. Its core tools are the mean–variance framework and allocation optimization based on correlations between assets. This line of thinking essentially turns investment and asset allocation into an engineering optimization game rather than an exploration based on real asset analysis. More specifically, this asset allocation theory has a fundamental problem. As Taleb has pointed out, we cannot obtain an asset correlation structure that is stable and extrapolatable over time. Correlation coefficients are essentially historical statistics: they may reflect diversification benefits in normal periods, but under extreme scenarios or systemic shocks they often rapidly converge, so assets once regarded as “low-correlated” fall in sync and risk becomes concentrated rather than dispersed (worse yet, because financial history is short and data granularity problematic, we actually lack sufficient high-quality historical statistical data). Stanley Druckenmiller expressed a similar view in a Goldman Sachs presentation: risk models may operate well in normal environments; but when markets enter a state of “total chaos,” asset correlations experience structural breaks and historical statistical relationships rapidly fail. Paradoxically, the models fail precisely at the moments of greatest risk. In other words, within the framework of modern portfolio theory, portfolio construction depends on past correlation structures, while the decisive moments are often the instants when correlations shift. Therefore, in extreme scenarios, relying on quantitative risk measures based on modern portfolio theory is not only insufficient but may provide a false sense of security.

Swensen’s doctoral advisor at Yale was James Tobin, the 1981 Nobel Prize laureate in economics, so he inevitably absorbed influence from the mainstream economics academic circle that emphasises the normal distribution assumption. For example, in the book he still tends to argue that capital market returns and risks largely follow a normal distribution; I do not fully agree with this. If return distributions are statistically stable, symmetric, and have controllable tails, then means and variances are indeed sufficient to characterise most risk features, and correlation coefficients become more operational. But real markets are clearly closer to heavy-tailed, skewed, and state-dependent distributions. The probability of extreme loss is often significantly higher than implied by the normal distribution, and what truly determines the fate of a portfolio are these low-frequency but high-impact events.

Empirically, asset correlations rise significantly during financial crises, volatility clusters, and tail co-movements are far higher than during normal periods. In the 2008 global financial crisis, equities, commodities, credit, and other risky assets dropped in high synchrony; in the early 2020 pandemic shock, most asset classes saw correlations rapidly converge in a short period. These structural breaks are not statistical noise but the result of the joint action of institutions, leverage, and liquidity constraints. In such circumstances, an “optimal portfolio” constructed from a historical mean–covariance matrix often loses explanatory power when an exogenous shock arrives.

Moreover, when considering Swensen’s allocations, one must note that the tax-exempt status of endowments provides an important advantage for his strategy: because of tax exemption, endowments can rebalance portfolios more frequently. This is a condition that most individual investors and many institutions cannot replicate.

Investment from a Fiscal Perspective: The Relationship between Consumption and Investment

Of course, these points are not the main focus of this article. Although I remain cautious about asset allocation theory itself, Pioneering Portfolio Management has provided me with deep inspiration. In my view, the most insightful part of the book is not the specific choice of asset classes but Swensen’s institutional exposition of the relationship between consumption and investment. Swensen defines university endowments as an intergenerational resource allocation institution whose central problem is not how to maximize wealth but how to balance current and future beneficiaries’ spending without damaging the long-term capital base. This sharply contrasts with Buffett-style investment logic. Buffett manages a holding company whose objective can be approximated as long-term compound growth of capital; consumption is not a constraint and capital growth is the ultimate goal. By contrast, in the Yale model capital is merely a means to serve consumption (to fulfill the educational mission). Investment decisions must embed explicit spending rules, such as maintaining real purchasing power, controlling the annual spending rate, and preserving intergenerational fairness across market cycles (ensuring future scholars can enjoy the same inflation-adjusted consumption as current ones). Theoretically, this aligns more with an intertemporal optimal consumption model rather than merely an asset-pricing or stock-picking problem. Thus Swensen’s investment perspective is not “how to accumulate more wealth” but “how to allocate consumption rights reasonably under uncertainty.” For him, asset allocation is a long-term fiscal arrangement serving institutional objectives. This positioning of the consumption–investment relationship deeply inspired me and forced me to reexamine investment from the perspective of its purpose.

I believe that for most ordinary people, the ultimate purpose of investment is not infinite expansion of asset size but to enhance present or future consumption. In other words, investment is a means and consumption is the end. On this point, Buffett’s path is highly special: he maintained very low personal consumption for a long time, reinvesting almost all disposable resources back into the capital system to maximise the compounding effect. Mathematically, the power of compounding depends not only on the rate of return but also on the capital retention rate. Buffett’s ability to achieve extreme long-term compounding essentially stems from his having minimised “consumption constraints” for decades so that capital was almost fully rolled over. Therefore, when we study Buffett’s astonishing long-term returns, if we focus only on investment decisions themselves and ignore his near-absence of consumption, the analysis is incomplete. Compound growth results from the joint action of return rate, time horizon, and capital retention. Even with identical returns, continuous withdrawals during the period produce exponentially different terminal values.

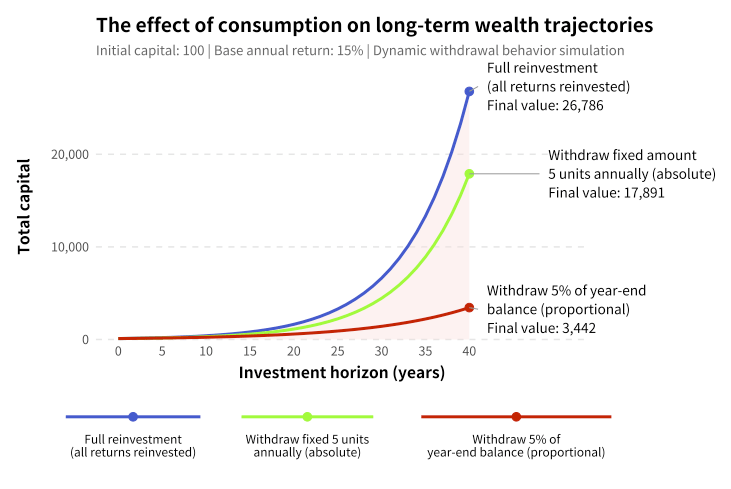

A simple comparison may help. As shown in the figure below, with initial capital 100, nominal annual return 15%, and investment horizon 40 years, different withdrawal rules produce markedly different wealth trajectories. If all returns are reinvested, capital compounds at 15% and the terminal value is about 26,786. If each year you first grow by 15% and then withdraw 5% of the year-end total, the terminal value is only about 3,442. If each year you grow first and then withdraw a fixed 5 units of cash, the terminal value is only 17,891. The results show that under the same nominal return, withdrawal rules and consumption paths have a very large effect on long-term capital accumulation. Whether capital is “interrupted” by continuous consumption and the specific form of that interruption often matters far more than differences of a few percentage points in returns.

It should also be noted that small improvements in returns are usually much harder to achieve than reductions in spending. Allow me to quote a passage from The Psychology of Money:

High savings rates mean you spend less than usual, and low spending means you save more than when you spend more. By contrast, many professionals spend countless hours and large sums of money on research just to increase investment returns by 0.1%. Put this in context and consider thrift and efficiency, and it becomes clear which approach is more important and worth pursuing. On one hand professional investors spend 80 hours a week researching investments just to gain 0.1 percentage points of return; on the other hand, these people’s economic lives have two or three percentage points of leeway, and they do not need to put in as much effort as in the first case—merely adjusting lifestyle slightly can make full use of that space.

More interestingly, consumption behavior itself affects your conception of “risk.” The definition of risk is a core dividing line between modern portfolio theory and value investors. Modern portfolio theory defines risk as return volatility, usually measured by variance or standard deviation. Under this framework, the greater the price fluctuation, the higher the risk; the lower the volatility, the lower the risk. Risk is treated as a statistical attribute: the dispersion of asset prices around expected returns. But to value investors, the essence of risk is permanent loss of capital, not price oscillations. Short-term price declines do not necessarily imply risk. As long as a firm’s intrinsic value is intact, buying during price declines may even lead to higher future returns. The real and sole risk is capital’s permanent impairment due to overpaying at purchase, fundamental deterioration, or being forced to sell at an inopportune time.

Returning to practical examples, if your spending depends on investment accounts like a university endowment, price volatility will more directly affect wealth. Continuous spending may force you to sell when asset prices are low to obtain cash, causing permanent capital loss. In such cases market declines are no longer mere statistical “volatility” but produce substantive shocks to wealth; volatility thus converts into real, permanent capital loss. Conversely, low consumption both increases capital retention and reduces the probability of forced sales. For ordinary investors, once living expenses depend on investment accounts, they may passively reduce positions during market downturns, converting short-term volatility into permanent capital losses. This explains why Duan Yongping repeatedly emphasizes that value investing should be done with idle money and not treated as a source of cash flow. With idle money, investors are more likely to be in a long-term “no need to liquidate” state like Buffett, which is crucial for risk management. In other words, differences in the understanding of risk fundamentally arise from differences in cash flow structure and consumption arrangements between individuals and institutions. For high-savings, low-fixed-expenditure investors, price volatility and low liquidity may not constitute risk; for highly leveraged, consumption-rigid investors, volatility and liquidity are more likely to trigger forced discounted sales and thereby cause substantive damage to wealth. Looking at Buffett again, it is incomplete to attribute his success merely to exceptional stock-picking ability or market judgment. Buffett’s investment system is built on an important premise: consumption is postponed almost indefinitely and capital can operate in a highly closed system.

One can also add a remark about differences between individual and institutional investors. For individual investors, the greatest structural advantage is more stable capital that does not have to withstand redemption pressure from external capital. This means individual investors can base investment decisions on long-term value judgments without being accountable for short-term paper volatility. By contrast, institutional investors, even if ideologically long-term, are often constrained by their capital structure. Most fund managers manage LPs’ money, and LP behaviour itself exhibits clear cyclicality: when markets perform well, inflows accelerate; when markets are weak, redemption pressure rises. Redemptions mostly occur when asset prices are low and often force managers to sell assets at low prices, causing permanent capital loss. Berkshire Hathaway (and some closed-end funds like Pershing Square) enjoys the advantage of a certain “permanence” in its capital structure: the company has no redeemable LP funds, and dissatisfied shareholders can only sell shares on the secondary market rather than directly withdraw company capital. Therefore, when the market falls, the balance sheet will not be passively reduced and the company does not need to liquidate assets at low prices to meet redemptions. Hence, if individual investors want to truly leverage their advantage, they should not compete with institutions on information channels, leverage scale, or trading speed—these are institutional strengths. Individuals’ more realistic and sustainable advantages lie in capital stability, lack of redemption pressure, and the ability to hold long term; reducing expenditure can further strengthen this advantage. Rather than imitating institutions’ strengths, use your freedom in time horizon and capital structure.

Why Do We Consume? Signalling, Identity, and Veblen’s The Theory of the Leisure Class

Overall, investment and consumption are two ends of the same system rather than two independent decision frameworks. Swensen’s real contribution to the Yale Endowment is not in asset allocation techniques per se but in redefining investment as “how to carry out intertemporal consumption arrangements without damaging the long-term capital base.” From the consumption perspective one can also see the hidden premise of Buffett-style wealth accumulation: near-zero consumption allows capital to be fully reinvested.

But here we must ask a more fundamental question: why do we consume? Housel’s observations in The Psychology of Money reveal many strange motives behind people’s consumption: we want to use consumption to show others that we deserve admiration and respect. People buy Ferraris to get admiring looks; ironically, when you drive a Ferrari the onlookers’ admiration is often not for you as a person but for the imagined scenario of themselves behind the wheel. The admiration and recognition you buy with wealth often never truly belong to you. Much consumption’s core driving force is not the utility the object itself brings but the signal it sends to others (and to oneself) about identity, status, and success.

Veblen noted in The Theory of the Leisure Class that the social function of consumption is not merely satisfying physiological needs but importantly establishing social status by displaying payment capacity. The leisure class engages in conspicuous wasteful consumption, purchases goods far beyond practical value, and engages in nonproductive leisure activities precisely to send a clear signal to society: I have resources that free me from the need to labor for a living. In this framework, consumption is essentially a social competitive tool rather than a pure economic decision. Signalling theory explains the mechanism: an effective signal must be costly—the signal sender must pay a real cost so that imitators cannot easily fake it. Luxury cars, designer watches, and high-end goods become identity signals because their high prices constitute an entry barrier.

But the question is: do we really need to participate in this competition? When consumption is internalised as a tool for self-identity and social comparison, individuals enter a typical “positional game.” In this game, payoffs depend on relative ranking rather than absolute levels. An increase in one party’s status often comes at the relative decline of others. Therefore, no matter how much total resources are invested, the group’s overall ranking structure does not change. This is a typical zero-sum or near-zero-sum competition whose equilibrium often exhibits “over-investment,” akin to an arms race: given others’ behaviour, each participant chooses to increase spending, ultimately forming a costly Nash equilibrium from which no one truly gains a net benefit; this equilibrium is inferior to potential Pareto-optimal states. In such cases, quitting becomes a wiser strategic choice. By refusing to participate in positional games, individuals can withdraw resources from relative-ranking consumptive competition and reallocate them to increase absolute wealth and long-term freedom. In other words, truly rational strategy is not to fight to win the finite game of consumption one-upmanship but to keep attention and resources focused on the infinite game that truly matters—the endless process of wealth accumulation.

Leave a comment